Copper Fundamentals to Undergo Significant Tightening in 2024?

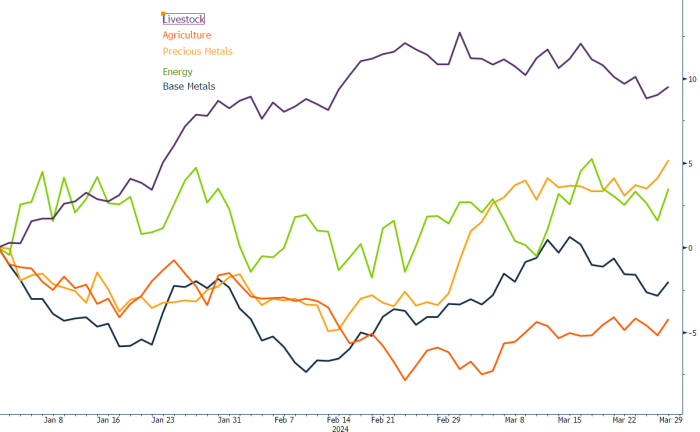

Commodity Price Performance By Asset

Source: Bloomberg, StoneX

Base metals concluded the first quarter of the year as the second worst performing commodity asset (above agriculture), with macro headwinds largely dominating price action (to read our recent article on the outlook for the macro economy over Q2, please click here ‘Underlying Fundamentals Will be the Area to Watch in H2’). Meanwhile, if we look at the individual price performances in the suite over the period, tin, nickel and copper were the only metals to record gains, with supply-side tightness a key common theme. Indeed, while nickel and tin received price support earlier in the year from the delayed issuance of Indonesia mining permit licences (KRABs), the country’s vow to accelerate the release of these permits resulted in both these metals recording peak quarterly prices by mid-March. However, in the case of copper, in our view the supply-side tightness story is only getting started. In this article we will discuss our view on copper in the quarter ahead and the reality behind recently announced Chinese smelter cuts.

Key Drivers Behind Copper’s Price Rally

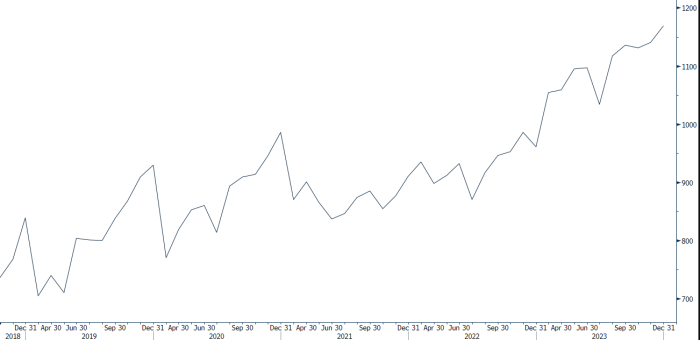

Copper LME 3M Price Performance

Source: Bloomberg, StoneX

Despite copper ending the first quarter of the year as the second best performing base metal (behind tin) up 3.6% over the period, the majority of price gains were accrued in the month of March, where copper briefly moved over its psychological $9,000/t level, before modestly pulling lower. As it stands at the start of Q2, copper is hovering around its highest level in a year.

The key driver behind higher prices has come from growing concerns over the availability of copper ore, particularly in China, due to the rapid deterioration in spot Treatment Charges (TCs), which have fallen from a seven-year high in November 2023, down to their lowest level since 2021. However, it is not just the outright level of TCs that a concern, but the pace of declines, falling almost 40% in Q1 2024, versus just 13% in Q4 2023. As a result, China’s Copper Smelters Purchasing Team (CSPT) which is a non-government led organisation combining ~ 85% of domestic smelter output, announced in its latest quarterly meeting that it would not set a reference figure for the spot TC in Q2, stating copper concentrate had “seriously deviated from the market fundamentals”.

Copper Treatment Charge

Source: Bloomberg, StoneX

Background - What Has Driven Chinese Spot TCs to Multi-Year Lows?

The Dynamics of TCs and Refined Supply – Flow Chart

Source: Bloomberg, StoneX

1. Chinese copper concentrate imports are undergoing greater growth than refined metal.

Chart One

Source: Bloomberg, StoneX

2. The key driver behind this has been not only higher demand in the country, but China’s desire to increase its domestic output (reducing its reliance on imported refined material).

Chart Two

Source: Bloomberg, StoneX

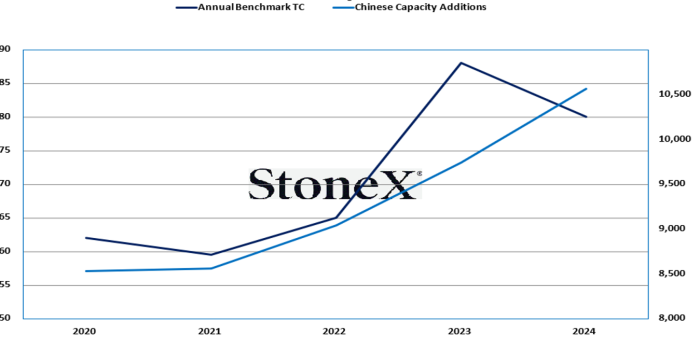

3. However, the drop in TCs of late is not just driven by capacity additions (see chart 3, which shows how annual annual benchmark TCs have been rising the last three years, despite capacity additions).

Chart Three

Source: Bloomberg, StoneX

4. Therefore, the recent fall in TCs and indeed decline in annual benchmarks is being driven by the sudden barrage of production guidance cuts in addition to the surprise news over First Quantum's Panama mine (given that China has opened itself up to rely more heavily on copper concentrate imports). Please note, reduced production guidance has arisen from a from a host of major producers such as Codelco and Anglo American facing either political and social obstacles, or more structural issues such as aging mines and falling ore grades. We have seen 600,000t+ removed from the copper concentrate side, or ~2.7% global output (if not more) and this has reduced the level of copper expected to be coming into China.

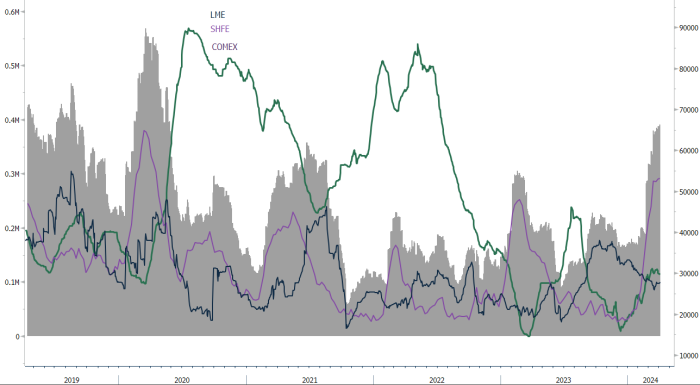

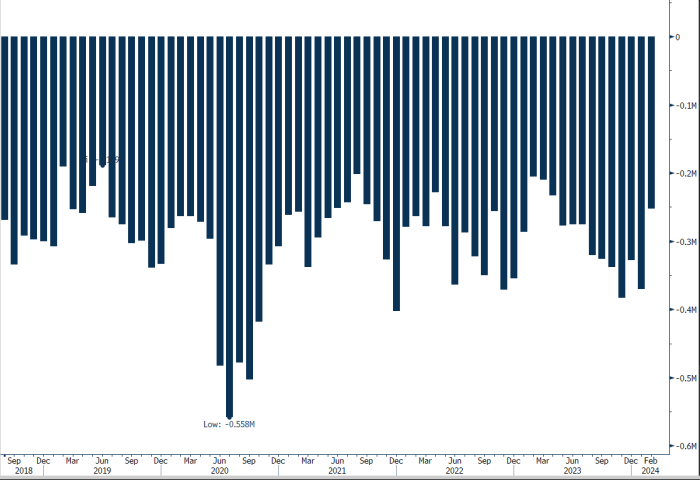

Apparent Tightness in Copper Concentrate is Not Being Reflected on the Refined Side… Yet?

Despite the headlines and indeed falling TCs highlighting the tightening supply of copper concentrate in the market, on the refined side, tightness is yet to be reflected on the same scale. Indeed, if we look at visible global exchange stocks they are at their highest level since May 2020, with the build of deliverable copper on the SHFE (on a seasonality basis) holding well above five-year averages. Further zooming into China, imports of copper cathodes are currently at a discount, while refined domestic production over January and February is up 11% Y/Y (with SMM forecasting a 2% M/M rise in output in March).

Chinese Refined Copper Production

Source: Bloomberg, StoneX

Global Visible Exchange Stocks

Source: Bloomberg, StoneX

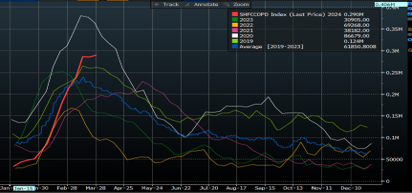

SHFE Copper Deliverable Stocks - Seasonality Chart

Source: Bloomberg, StoneX

Net Imports of Refined Copper into China

Source: Bloomberg, StoneX

But What About Reported Cuts From CSPT?

On 28th March, CSPT held its quarterly meeting with the following outcomes:

1. In view of the fact that the current spot TC/RC of copper concentrate has seriously deviated from the market fundamentals, in order to take effective measures to promote the spot TC/RC to return to a reasonable level, the meeting decided not to set a reference figure for the spot TC/RC of copper concentrate in the second quarter.

2. Establish a supplier blacklist mechanism and advocate CSPT companies not to cooperate with blacklisted companies.

3. Initiate CSPT companies to jointly reduce production by 5-10%, and promote implementation.

4. Expand the scale of the CSPT and invite large-scale enterprises outside the team to join the CSPT.

5. Prepare to hold a special meeting on inspection work, invite professional inspectors from various enterprises to share and exchange inspection results, and promote fairness and fairness in inspection work.

Understandably market attention is focused on the potential for upcoming smelter cuts (of 5-10%), following previously vague parameters set out to reduce production in an earlier March meeting known as the Copper Smelting Enterprise Symposium (consisting of 19 main leaders of domestic smelting companies and relevant national Ministries/Commissions). However, despite the CSPT confirming a target level for cuts, given the group is non-Governmental, we expect that achieving this target ‘optionally’ will be challenging. Indeed, we’ve already heard from two of the largest smelters in the country who have spoken out. Firstly, Jiangxi Copper announced in its earnings report on 27th March that production this year will rise 11% to a new record high, while Tongling Nonferrous Metals has been vocal in stating that it won’t cut output or change its maintenance schedule on lower TCs. Furthermore, it is worth noting that provincial Governments will favour expanding growth from local industries, while many of the largest smelters in the country remain profitable on term TCs (which stand just 9% below 2023 levels at $80/t).

So Where Does This Leave Copper’s Fundamentals and Price?

Despite our view that copper smelter cuts are less dramatic than headlines suggest, we do support the outlook that the copper market will tighten on the refined side in the months ahead, providing price support. Firstly, over Q2 we expect China to enter its peak maintenance period, in addition to the outlook for domestic and foreign demand likely to improve from its current levels. Arguably here, a recovery in the demand outlook for copper is pivotal when it comes to price forecasting in 2024, with the supply-side and its constraints better understood. Looking at demand itself, we continue to forecast that copper’s applications within the green transition will outpace that of traditional demand sectors, with China’s property market a key headwind over the year. Please see our market balance below.

Copper Market Balance

Source: Bloomberg, SMM, BLC, StoneX

Definitions

Chinese Smelter Purchase Team (CSPT): A group of China’s top copper smelters (which together account for ~80% of domestic output). In charge of setting annual and quarterly TCs.

Treatment Charge (TC): The fee paid to smelters by miners for converting copper concentrate to copper cathode.

The StoneX Group Inc. group of companies provides financial services worldwide through its subsidiaries, including physical commodities, securities, exchange-traded and over-the-counter derivatives, risk management, global payments and foreign exchange products in accordance with applicable law in the jurisdictions where services are provided. References to over-the-counter (“OTC”) products or swaps are made on behalf of StoneX Markets LLC (“SXM”), a member of the National Futures Association (“NFA”) and provisionally registered with the U.S. Commodity Futures Trading Commission (“CFTC”) as a swap dealer. SXM’s products are designed only for individuals or firms who qualify under CFTC rules as an ‘Eligible Contract Participant’ (“ECP”) and who have been accepted as customers of SXM. StoneX Financial Inc. (“SFI”) is a member of FINRA/NFA/SIPC and registered with the MSRB. SFI is registered with the U.S. Securities and Exchange Commission (“SEC”) as a Broker-Dealer and with the CFTC as a Futures Commission Merchant and Commodity Trading Adviser. References to securities trading are made on behalf of the BD Division of SFI and are intended only for an audience of institutional clients as defined by FINRA Rule 4512(c). References to exchange-traded futures and options are made on behalf of the FCM Division of SFI . StoneX is a trading name of StoneX Financial Ltd (“SFL”). SFL is registered in England and Wales, Company No. 5616586. SFL is authorized and regulated by the Financial Conduct Authority [FRN 446717] to provide to professional and eligible customers including: arrangement, execution and, where required, clearing derivative transactions in exchange traded futures and options. SFL is also authorised to engage in the arrangement and execution of transactions in certain OTC products, certain securities trading, precious metals trading and payment services to eligible customers. SFL is authorised & regulated by the Financial Conduct Authority under the Payment Services Regulations 2017 for the provision of payment services. SFL is a category 1 ring-dealing member of the London Metal Exchange. In addition SFL also engages in other physically delivered commodities business and other general business activities which are unregulated and not required to be authorised by the Financial Conduct Authority. StoneX Group Inc. acts as agent for SFL in New York with respect to its payments services business. StoneX APAC Pte. Ltd. acts as agent for SFL in Singapore with respect to its payments services business. ‘StoneX’ is the trade name used by StoneX Group Inc. and all its associated entities and subsidiaries.

Trading swaps and over-the-counter derivatives, exchange-traded derivatives and options and securities involves substantial risk and is not suitable for all investors. Past performance of any futures or option is not indicative of future success. Indicators are not a trading system and are not published as a specific trade recommendation. The information herein is not a recommendation to trade nor investment research or an offer to buy or sell any derivative or security. It does not take into account your particular investment objectives, financial situation or needs and does not create a binding obligation on any of the StoneX group of companies to enter into any transaction with you. You are advised to perform an independent investigation of any transaction to determine whether any transaction is suitable for you. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of StoneX Group Inc.

© 2024 StoneX Group Inc. All Rights Reserved.

Discover more insights